Vesting Schedules Explained for Private Companies

February 26, 2026

When companies grant equity, they aren’t just giving away ownership. They’re making a long-term promise — one that ties the success of the business to the commitment of its people. The way that promise is structured is called a vesting schedule, and it can have a bigger impact on incentives, retention, tax exposure, and accounting outcomes than most people realize.

In this blog, we’ll break down what a vesting schedule is, why it matters from both a corporate and tax perspective, and how different mechanisms — like cliffs, leave pauses, performance triggers, double triggers, and two-tier RSUs — play out in practice. We’ll also explore how small drafting details can create major financial consequences, and we’ll close with practical takeaways on why precision and tracking are non-negotiable.

What Is a Vesting Schedule?

A vesting schedule defines when and how employees, advisors, founders, or executives earn their equity compensation — whether stock options, RSUs, or restricted shares.

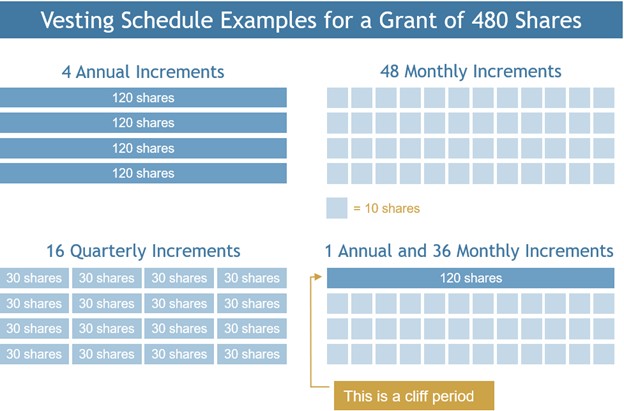

Instead of granting ownership outright, companies divide equity into installments (often called tranches) that vest over time. An employee might receive a grant of stock options but earn the right to exercise them gradually —typically vesting schedules include monthly vesting, quarterly vesting, annually vesting or cliff vesting.

For the company, this protects the cap table and aligns incentives with long-term contribution and prevents short-term hires from leaving with ownership before demonstrating commitment and fit.

For the employee, it creates a visible and accumulating reward for continued impact while also functioning as a trial period. If the employee leaves before the vest date, they forfeit the grant.

Vesting schedules are not just administrative timelines — they are structural incentive systems embedded in compensation design.

Illustration of Vesting Schedules

Vesting Commencement Date: Why The Clock Matters

The vesting commencement date is when the vesting clock officially starts ticking.

It often matches the hire date — but not always.

Some companies use:

- The board approval date

- The offer acceptance date

- A performance milestone date for executive or founder grants

This distinction matters. The vesting commencement date determines when the grant expires and when the first tranche vests. A discrepancy of even a few days between the offer letter and the board resolution can determine whether an employee vest shares upon termination — or walks away with nothing.

Consistency across grant agreements, board approvals, and internal systems is critical.

Vesting Variations: Performance and Life Events

Not all vesting is linear or purely time-based. Real business conditions — and real life — often intervene. These scenarios are not merely design variations; they meaningfully challenge stock administration and tracking, requiring systems that can handle pauses, performance conditions, layered triggers, and precise recalculations without error.

Performance Vesting

Some grants require the achievement of specific milestones before vesting occurs.

Examples include:

- A sales leader’s equity tied to reaching $10M in ARR

- An R&D executive’s grant linked to regulatory approval or product launch

- Founder shares that vest upon achieving a valuation multiple

Performance vesting tightly aligns equity with measurable outcomes. But it must be drafted carefully. Objectives must be clearly defined, measurable, and verifiable. Ambiguity invites disputes — especially when the equity value becomes significant.

Pausing Vesting: Leave of Absence (LOA)

One often overlooked feature is what happens during a leave of absence.

Many sophisticated equity plans include “tolling” provisions that pause vesting during unpaid leave. If an employee takes six-month unpaid leave and tolling applies, the vesting schedule freezes and resumes only upon return — pushing the final vesting date out accordingly.

This detail can materially affect both tax timing and employee expectations. Companies need to clearly define:

- Which types of leave pause vesting

- Whether paid leave is treated differently

- How partial months are handled

This is not only required for administrative purposes, but also to ensure the company meets employment law requirements across different jurisdictions.

Acceleration: Speeding Up the Timeline

Acceleration refers to speeding up vesting ahead of schedule, typically triggered by major corporate events such as an acquisition or IPO.

There are two common structures:

Single Trigger: Vesting accelerates immediately upon a change of control. This is rare for broad employee populations but may apply to founders or select executives.

Double Trigger: The industry standard for employee protection.

Two conditions must occur:

- A change of control (e.g., acquisition)

- A qualifying termination, typically termination without cause or resignation for “good reason,” within a defined period after the transaction

Only if both conditions occur does vesting accelerate.

For employees, this provides protection against being “cleaned out” by an acquirer if their role is eliminated following a transaction.

For companies, it ensures employees who are at risk of termination remain incentivized and engaged through the transition.

Importantly, acceleration does not add a new vesting condition — it simply speeds up time-based vesting that would have occurred anyway.

These structures reflect the core mechanics of stock option vesting — but when companies shift to RSUs, the complexity often increases.

RSUs vs. Options: Why the Structure Changes the Risk Profile

As companies mature, many shift from stock options to RSUs.

Stock options follow a relatively straightforward logic:

- Vesting gives the employee the right to purchase shares.

- If the employee leaves before vesting, unvested portions are forfeited.

- Tax is generally triggered only when the employee chooses to exercise (depending on jurisdiction and option type).

Options give employees control over timing and allow companies to maintain a relatively linear administrative structure.

RSUs operate differently. While at first glance they may seem simpler and more employee-friendly — no exercise price, no decision about when to exercise, and a clearer perception of value — that difference introduces additional layers of complexity.

RSUs can be highly effective. But here’s the practical reality: RSUs don’t just create value — they can also create recurring tax exposure as each tranche vests.

That’s the classic “tax without liquidity” problem — and in private companies, it can repeat year after year.

Because of this, companies often attempt to address the liquidity mismatch through a two-tier structure.

Two-Tier Vesting: A Practical Solution with Real Tradeoffs

In private companies, RSUs are frequently structured with two layers:

- Tier 1: Time-based vesting (service condition)

- Tier 2: A liquidity trigger (IPO, acquisition, or tender offer)

The logic is straightforward: RSUs only become deliverable once liquidity exists, aligning the tax liability with an actual opportunity to monetize the shares. Unlike acceleration, this structure adds an additional vesting requirement. Shares are not considered fully vested until both conditions are satisfied.

In many jurisdictions, this can be an effective way to prevent employees from paying tax on illiquid equity. However, it may create challenges in qualifying for favorable tax regimes and can limit employees’ ability to become actual shareholders and benefit from capital gains treatment in certain jurisdictions.

Also, two-tier vesting introduces real structural and operational challenges — especially when compared to traditional stock options. It adds a second condition that must be monitored, interpreted, and administered — typically tied to a future corporate event that may be uncertain in both timing and structure.

For example:

- If the liquidity event is far off, employees may wait years for settlement. Liquidity becomes uncertain, raising additional questions around tax treatment and what happens to employees who leave before liquidity occurs.

- If liquidity is already imminent at the time of grant, tax authorities may question whether the second tier is genuinely substantive.

- Operationally, tracking becomes significantly more complex. Each tranche must be monitored against both service completion and the occurrence (or non-occurrence) of a liquidity event.

Two-tier RSUs can be an elegant solution to a real liquidity problem. But compared to stock options, they require more deliberate drafting, tighter compliance controls, and more sophisticated stock administration.

Stock-Based Compensation and Accounting

Something people are often not aware of: equity design decisions ripple directly into accounting.

Different vesting structures — particularly those involving performance conditions — change how expense is recognized under ASC 718 (U.S.) or IFRS 2 (international standards).

Performance-based awards, market conditions, and liquidity triggers each carry distinct recognition and measurement implications.

In other words, equity design is not just an HR decision — it is a finance, tax, and compliance decision.

Key Takeaways

- Tranches are micro-events: Vesting is not one event — it’s a series of discrete tranches. Each one affects tax timing, employment status, and cap table accuracy.

- Precision is critical: Rounding rules, day-count conventions, tolling mechanics, and trigger definitions can materially change outcomes. Small drafting inconsistencies lead to big discrepancies.

- Creative structures carry consequences: Double triggers, performance accelerations, and two-tier RSUs are powerful tools — but each introduces legal, tax, and accounting complexity.

- Tracking is non-negotiable: Designing a vesting schedule is only the beginning. It must be tracked accurately at the tranche level, reconciled with board approvals, and clearly communicated to employees.

The Bottom Line

Vesting schedules are the DNA of equity compensation. They translate ownership into motivation and effort into reward. They align commitment with company growth.

But they are also complex legal and financial instruments that demand precision.

If you’re building or revising an equity plan, treat vesting schedules as strategic architecture — not boilerplate language. The structure you choose will shape incentives, tax exposure, accounting outcomes, and employee trust.

If your company is granting equity, don’t leave vesting to spreadsheets. Get the structure right, stay compliant, and give your people the clarity and confidence they deserve.

A robust equity data model — built for the details that truly matter — should handle vesting with granular precision, from leave pauses and acceleration triggers to two-tier RSU structures and fractional share rounding.

For more resources for private companies, check out the Private Company Stock Plans section on NASPP.com

-

By Yarin Yom-TovProduct Tax Manager

Slice Global